ABC production analysis

ABC Analysis is a method of tiered inventory or supplier valuation that divides inventory/suppliers into categories based on cost per unit and quantity held in stock or turned over a period of time. This is one of the four methods of overall materials management and inventory management.

ABC analysis can often be confused with Activity Based Costing, a similar sounding term that refers to a method of manufacturing costing that is more refined than the traditional machine-hours method of determining the overhead cost of a finished product.

ABC-Production-Analysis

What is the Purpose of ABC Analysis?

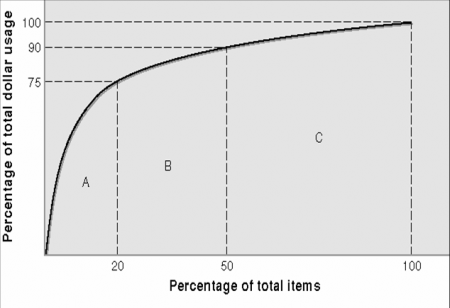

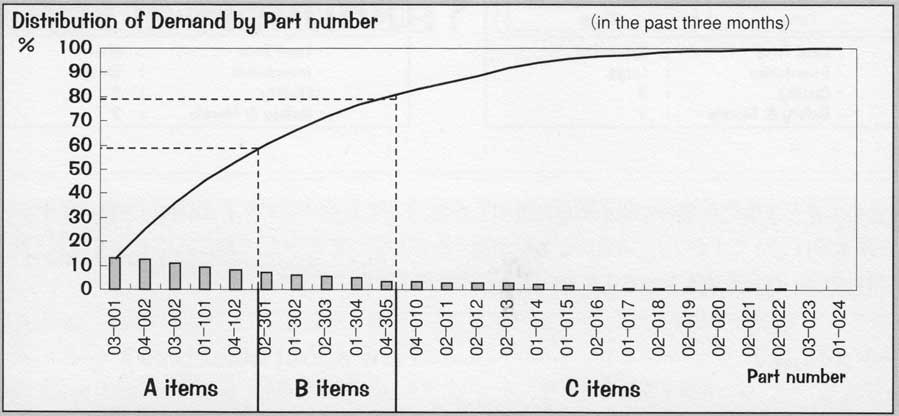

ABC Analysis allows inventory/purchasing managers to segregate and manage the overall inventory/suppliers into three major groups. This allows different inventory/supplier management techniques to be applied to different segments of the inventory/suppliers in order to increase revenue and decrease costs. In terms of a Pareto Analysis, it separated the critical few from the trivial many.

“A” Category items generally represent approximately 15%-20% of an overall inventory by item, but represent 80% of value of an inventory. By paying attention close attention in real-time to the optimization of these items in inventory, a great positive impact is possible with minimal increase in inventory management costs.

“B” Category items represent 30%-35% of inventory items by item type, and about 15% of the value. These items can generally be managed through period inventory and should be managed with a formal inventory system.

“C” Category items represent 50% of actual items but only 5% of the inventory value. Most organizations can afford a relatively relaxed inventory process surrounding these items.

Comments